The Inter-American Center of Tax Administrations (CIAT) added a chapter to their Manual for Control of International Tax Planning on 1 November 2022. This chapter is about the introduction of a Cooperative Compliance programme by tax administrations in developing countries and is written by Diego Quiñones from Colombia and Irma Mosquera Valderrama and Esther Huiskers-Stoop from Leiden University.

CIAT is an international organisation specialised in training and exchanges of information between national tax administrations in Latin America and provides specialised technical assistance for the updating and modernisation of these tax administrations. The complete manual has 42 sections (new chapters will be published soon), which were prepared in coordination with 48 experts who have extensive experience in tax administrations, ministries of finance, international organisations, academia, civil society and private initiatives. The manual includes an analysis of the various risks of tax evasion and avoidance, based on behaviours of multinational companies as detected by tax administrations from various countries, as well as the possible actions to identify said risks and consequently treat them.

Section 5 provides tools for combating international tax planning and chapter 5.5 provides more specifically Cooperative Compliance Initiatives as a Preventative Mechanism. Cooperative Compliance in general can be defined as ‘the establishment of a trust-based cooperative relationship between taxpayers and the tax authorities on the basis of voluntary tax compliance leading to the payment of the right amount of tax at the right time’. The origins of Cooperative Compliance are found in the 2008 Report by the Organization for Economic Cooperation and Development (OECD) Forum on Tax Administration (FTA) on the Role of Tax Intermediaries. This study encouraged tax administrations to establish a relationship based on trust and cooperation with taxpayers (mainly large taxpayers) in order to tackle aggressive tax planning. These relationships are entered into voluntarily by taxpayers, and their voluntary and transparent regulatory compliance will be rewarded with more anticipated certainty and a reduction of (possible) subsequent tax audits, sanctions and prosecution. For such a relationship to exist, it is essential that tax administrations, taxpayers, and their tax intermediaries ‘start to trust each other’ and maintain that trust.

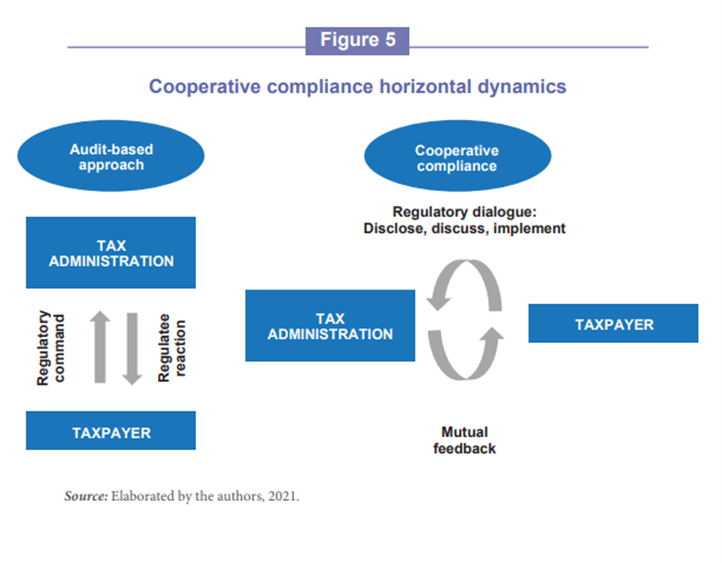

Chapter 5.5 answers critical questions such as: What are the goals and principles behind Cooperative Compliance? How does Cooperative Compliance work? What are the potential benefits and risks of cooperative enforcement in the context of developing countries? and more. Tax administrations considering implementing a Cooperative Compliance programme, will need to evaluate the changes that will need to take place: before, during the design, and after the introduction of the programme. These changes may be different among countries, and therefore, a self-evaluation by each tax administration will need to take place before introducing the programme. Therefore, the authors distinguish 18 building blocks to pave the way for a Cooperative Compliance approach. Furthermore, the chapter contains diagrams to facilitate understanding of the operation of Cooperative Compliance models. For example, the following graph, found on page 27, shows the change in dynamics between control processes based on coercive actions (left) and cooperative compliance (right).

Changing views on tax enforcement, tax compliance, and tax planning require continual reflection on further improvements of the concept of Cooperative Compliance. This manual will be useful for all those interested in learning or strengthening their knowledge on these subjects.

Read the full chapter, available in English 5.5. Cooperative Compliance Initiatives as a Preventative Mechanism | Inter-American Center of Tax Administrations (ciat.org) and Spanish 5.5. Iniciativas de cumplimiento cooperativo como mecanismo preventivo | Centro Interamericano de Administraciones Tributarias.

This post was also published on the LeidenLawBlog.